Landscaping insurance is an umbrella term. Landscaping insurance is a bundle of commercial insurance policies that protect landscaping businesses from various risks, such as lawsuits, property damage, equipment theft, and pollution liability.

Landscaping insurance can cover legal fees, repair costs, replacement costs, and awarded damages. Apart from covering damages and protection from claims, landscapers can bid on contracts. The certificate can satisfy the eligibility of commercially contracted, informed landlords.

Landscaping insurance is not mandatory by law in Canada, but it is highly recommended for landscapers who want to safeguard their financial assets and reputation.

Landscaping insurance rates vary depending on the business’s size, scope, and location, but they can start as low as $500 per year for a $1 million coverage.

Commercial General Liability Insurance (CGL), a type of insurance under landscaping insurance, might not be required by law. However, it is generally required by commercial offerors, landlords, and other contractors who subcontract.

Moreover, WSIB (Workplace Safety and Insurance Board) is mandatory for most businesses in Ontario. This means that if you have employees in Ontario, you are required to register with the WSIB and pay premiums. The exception is that you MUST be exempt if you have fewer than 10 employees!

Insurance can save your landscaping business from liquidation

- Sprinkler Damage: Your lawn mower causes flooding on your customer’s lawn due to a damaged sprinkler system line.

- Equipment theft: When left overnight on site or in your vehicle, your equipment is taken.

- Commercial vehicle theft: Your commercial vehicle is taken from the site.

- Trip and fall: Despite warning signs, someone falls in the work area and is injured.

- Storage shed fire: Your equipment shed catches fire and is destroyed.

- Equipment breakdown: Equipment malfunctions during use and needs to be repaired.

- Commercial site vandalism: A commercial site you are working on is damaged by malicious acts.

- Herbicide/pesticide illness: A person or pet becomes ill due to the chemicals you use on a client’s property.

- Fertilizer/chemical damage: The fertilizer or chemicals you use to damage your client’s lawn, causing discoloration or other problems.

- Employee injury: An employee is hurt on the job and files a claim against you for damages.

- Employee theft: An employee takes something from one of your clients.

- Natural disaster damage: A natural disaster such as a flood or windstorm damages your office, equipment workshop, or computer.

- Object damage: Property is damaged by objects thrown by mowers and trimmers or by tree-trimming operations.

- Flood damage: The property is damaged due to flooding from a sprinkler system malfunction.

- Third-party claims/disputes: Your compensation is stuck due to a dispute between two parties.

List of Insurance Coverage a Landscaping Business Should Explore

This list is not to discourage you but to give you a sense of the available protections.

1. Commercial General Liability Insurance (CGL)

This type of insurance covers your business if you are sued for bodily injury, property damage, or advertising injury caused by your work. It is a basic insurance that all landscaping businesses should have.

2. Commercial property/Building Insurance

This type of insurance covers your business’s property against damage from fire, theft, vandalism, and other risks. It is essential to have this coverage if you own your business premises.

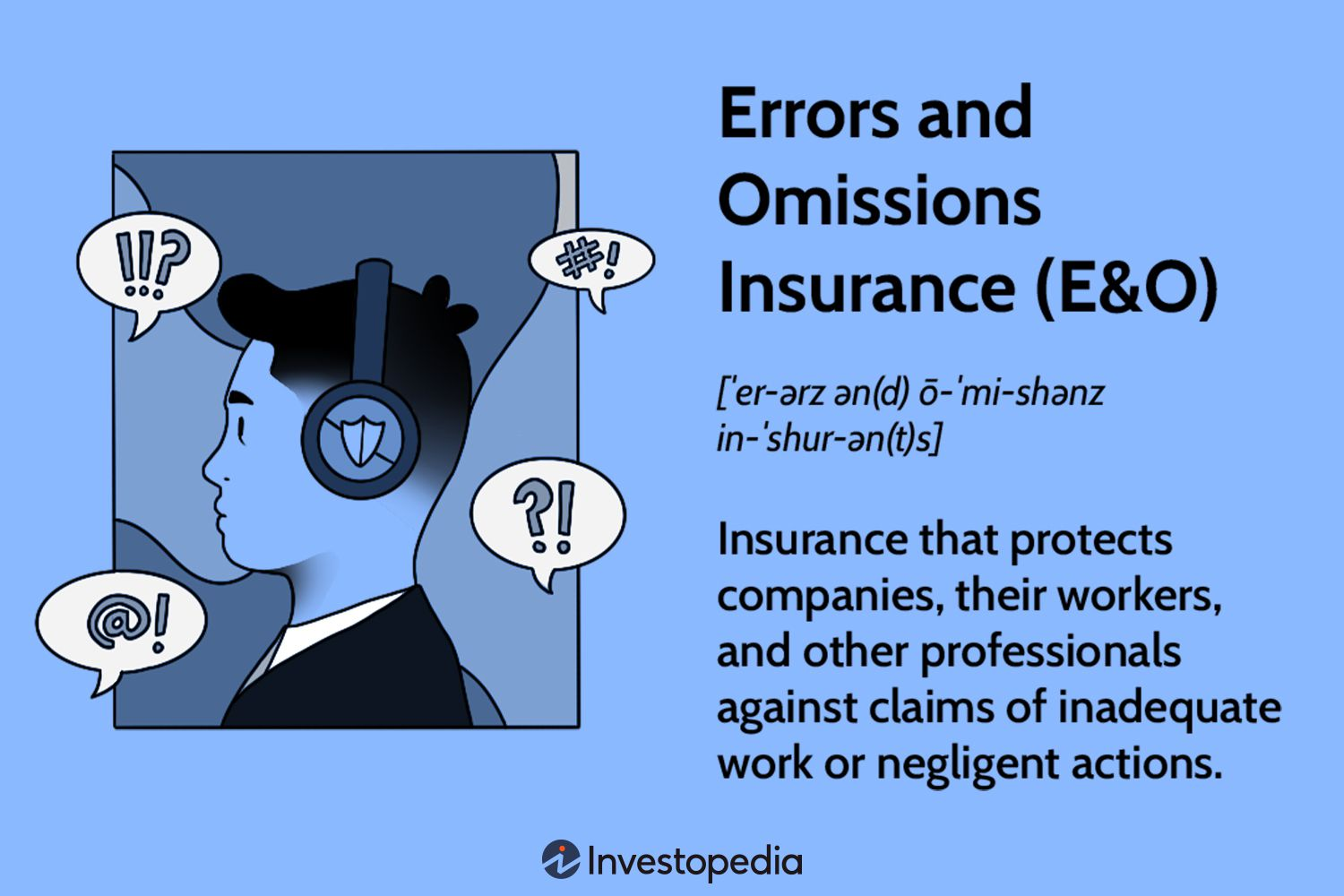

3. Professional Liability Insurance (AKA errors and omissions (E&O))

This type of insurance covers your business if you are sued for mistakes or errors made during your work. This is important for landscaping businesses that provide professional services, such as landscape design or irrigation installation.

4. Commercial Auto Insurance

This type of insurance covers your business’s vehicles against damage in the event of an accident. It is essential to have this coverage if you use vehicles for business purposes, such as to transport equipment or supplies.

5. Pollution liability

This type of insurance covers your business if you are sued for environmental damage caused by your work. This is important for landscaping businesses that use chemicals or other potentially harmful substances.

6. Tools And Equipment Coverage

This type of insurance covers your business’s tools and equipment against damage or theft. It is vital to have this coverage if you have expensive tools or equipment that are essential to your business.

7. Equipment Breakdown Insurance

This type of insurance covers your business for the cost of repairing or replacing equipment that breaks down. This is important for landscaping businesses that rely on specialized equipment to do their work.

8. Cyber Insurance

This type of insurance covers your business when dealing with a cyberattack, such as a data breach or ransomware attack. This is becoming increasingly important as companies become more reliant on technology.

9. Disability insurance

This type of insurance provides income replacement if you cannot work due to illness or injury. This is important for landscaping businesses that rely on the owner or key employees.

10. Life insurance

This type of insurance provides financial protection for your family if you die. This is important for landscaping businesses that want to ensure their families are cared for if something happens to the owner or key employees.

11. Workers’ compensation insurance

This type of insurance covers the cost of medical expenses and lost wages for employees who are injured on the job. It is mandatory for all businesses in Canada.

12. Installation floater

This type of insurance covers repairing or replacing damaged property while installing new equipment or systems. This is important for landscaping businesses that do a lot of installation work.

13. Legal Expense Insurance

This type of insurance covers the legal fees if you are sued. This is important for landscaping businesses that may be exposed to legal liability.

14. Group Health Benefits

This type of insurance provides health insurance coverage for employees. This is important for landscaping businesses that want to attract and retain good employees. Offering group health benefits shows you care about your employees and their well-being.

This can make your business more attractive to potential employees and help improve employee morale and productivity. It can also help employees save money on their healthcare costs, which can significantly attract and retain good employees, especially in today’s competitive job market.

Landscaping Insurance Pricing Estimates

The prices shown below are only estimates. The actual pricing depends on many factors mentioned below this section. Depending on your business, it is better to approach your agent or advisor for more accurate estimates.

- Commercial General Liability Insurance (CGL): $45-530 per year

- Commercial property/Building insurance: $1,500-3,000 per year

- Professional Liability Insurance (AKA errors and omissions (E&O)): $100-300 per year

- Commercial Auto Insurance: $150-1,810 per year

- Pollution liability: $100-300 per year

- Tools And Equipment Coverage: $100-300 per year

- Equipment Breakdown Insurance: $100-300 per year

- Cyber Insurance: $100-300 per year

- Disability insurance: $100-300 per year

- Life insurance: $100-300 per year

- Workers’ compensation insurance: $2,770-5,540 per year

- Installation floater: $100-300 per year

- Legal Expense Insurance: $100-300 per year

- Group Health Benefits: $1,500-3,000 per year

💡 A small company – less than 3 people lawn care business might pay an average of $2,000 for $2 million coverage annually.

General liability insurance would cost around $500, and Business property coverage would cost $100. Opting for worker’s compensation might set you back around $5- $6 for every $100 you pay. Apart from this, you might have equipment/installation floaters along with a professional liability cover.

💡Insurance companies also stipulate a per-occurrence limit and an aggregate limit. Your aggregate limit might be 2 million, but you can only claim your occurrence limit (1 million or less) in a single claim.

Your price depends on these factors:

- The cost of insurance can vary depending on where you are located. For example, businesses in areas with a high risk of natural disasters may pay higher premiums.

- The types of services you offer. For example, businesses that offer tree or snow removal may pay higher premiums than those that only offer lawn care.

- Your number of employees: Businesses with more employees typically pay higher premiums than businesses with fewer employees.

- The type of projects you work on: For example, businesses that work on commercial projects may pay higher premiums than businesses that only work on residential projects.

- Your business’s annual projected revenue: Businesses with higher projected revenue typically pay higher premiums than businesses with lower projected revenue.

- If you have a history of claims, your premiums will be higher. Insurance companies view businesses with a claims history as more likely to file future claims.

- The size of your business. Larger businesses typically pay higher premiums than businesses that are smaller.

- The value of your assets. Businesses with more assets typically pay higher premiums than businesses with fewer assets.

- The amount of experience you have in the industry can also affect the cost of insurance. Businesses with more experience typically pay lower premiums than businesses with less experience.

- The amount of payroll you expect to pay. Businesses with higher payroll estimates typically pay higher premiums than businesses with lower payroll estimates.

- If you use pesticides in your work, your premiums may be higher. Pesticides can be hazardous and lead to lawsuits.

- Your premiums may be higher if you offer additional services like snow removal or tree removal.

By understanding the factors that affect the price of landscaping insurance, you can help ensure that your business gets the best possible coverage.

Landscaping Insurance benefits

You get protection from:

- Harsh weather: Insurance can protect you from financial losses caused by storms, floods, and other weather events.

- Equipment theft & damage: Insurance can help you replace or repair stolen or damaged equipment.

- Workplace accident: Insurance can help cover medical expenses and lost wages if an employee is injured.

- Fire protection: Insurance can help cover repairing or replacing property damaged by fire.

- Lawsuits: Insurance can help protect you from financial losses if you are sued.

- Third-party bodily injury: Insurance can help cover medical expenses and lost wages if a third party is injured due to your work.

- Unappreciated employees: Insurance can help cover the cost of legal fees if an employee files a wrongful termination lawsuit against you.

- Disasters: Insurance can help cover the cost of repairing or replacing property damaged by a disaster, such as a hurricane or tornado.

- Advertising injury: Insurance can help cover the cost of legal fees if you are sued for libel, slander, or other advertising-related claims.

- Any other third-party claims: Insurance can help cover the cost of legal fees and damages if you are sued for any other type of third-party claim.

Why Need One?

🧪 Use of chemicals

Many landscaping tasks involve chemicals, such as pesticides, herbicides, and fertilizers. These chemicals can be hazardous if not handled properly and pose an environmental risk. Landscape insurance can help protect you from liability claims if someone is injured or if the environment is damaged due to your use of chemicals.

🏭 Heavy machinery

Landscapers often use heavy machinery, such as lawnmowers, tractors, and excavators. These machines can be dangerous if not operated properly and cause serious injury or property damage if they are involved in an accident. Landscape insurance can help protect you from liability claims if someone is injured or if the property is damaged due to your use of heavy machinery.

⛺ Working outdoors

Landscapers often work outdoors, which exposes them to various risks, such as falls, slips, and accidents involving power tools. Landscape insurance can help protect you from liability claims if someone is injured on your property while working.

🌳 Heavy trees

Landscapers often work with heavy trees, which can be dangerous if improperly handled. If a tree falls and injures someone or damages property, landscape insurance can help protect you from liability claims.

💼👩🏽💻🤝 Protects company, employees, clients

Landscape insurance can help protect your business, employees, and clients from financial losses. For example, if a client’s property is damaged during a landscaping project, landscape insurance can help cover the cost of repairs. Or, if an employee is injured on the job, landscape insurance can help cover medical expenses and lost wages.

💸 Financial disputes

Landscape insurance can help protect you from financial disputes with clients or suppliers. For example, if a client refuses to pay for a landscaping project, landscape insurance can help cover the project’s cost. Or, if a supplier fails to deliver materials on time, landscape insurance can help cover the cost of lost profits.

😳Unexpected losses

Landscape insurance can help protect you from unexpected losses, such as theft, vandalism, or natural disasters. For example, landscape insurance can help cover the replacement cost if your equipment is stolen. Or, if a storm damages your property, landscape insurance can help cover the cost of repairs.

🫶 Win contracts

Clients and general contractors often ask for proof of insurance before hiring a landscaping contractor. Having landscaping insurance can give you an edge in the competitive bidding process.

🚧Construction bond

A construction bond is a surety bond that is required for some landscaping projects. This bond protects the client if the contractor fails to complete the project or does not meet the agreed-upon standards. Landscape insurance can help you obtain a construction bond.

What happens when you do not have Landscaping Insurance?

Damages

If you are sued for damages caused by your landscaping work, you could be personally liable for repairs or medical expenses if someone is injured. Without landscaping insurance, you could be forced to pay these costs out of your pocket.

Legal fees

If you are sued, you will likely need an attorney to defend you. Legal fees can be expensive, and without landscaping insurance, you could be responsible for paying them all yourself.

Medical bills

If someone is injured due to your landscaping work, they may be able to sue you for medical expenses. These expenses can be significant; without landscaping insurance, you could be responsible for paying them all yourself.

Loss of project

If a client is unhappy with your work and they sue you, they may refuse to pay for the project. This could mean that you could not collect any money for your work and be responsible for paying the client’s legal fees.

Reputation

If you are sued for damages or if someone is injured due to your landscaping work, your reputation could be damaged. This could make it challenging to win new clients in the future.

Time

Dealing with a lawsuit can be time-consuming and stressful. This could take away from the time you spend running your business or working on landscaping projects.

Working capital

If you are sued or have to pay medical expenses, you could lose working capital. This could make it difficult to pay your employees, buy supplies, or cover other business expenses.

Financial disputes

If you have a financial dispute with a client or supplier without landscaping insurance, you could be personally liable for the costs of the dispute. This could include legal fees, court costs, and even damages.

In short, not having landscaping insurance can expose you to significant financial risk. If you are a landscape contractor, snow removal contractor, or lawn care professional, it is essential to have landscaping insurance to protect yourself and your business.

Who needs it?

This is not an exclusive list.

- Tree trimmers

- Landscape designers

- Land irrigation contractors

- Landscape architects

- Landscapers

- Arborist (tree surgeon)

- Groundskeepers

- Field technicians

- Well drilling contractors

- Tree removal pros

Things you should know if you are buying insurance for your landscaping business

Certificate of Insurance (COI)

A COI (Certificate of Insurance) is a document issued by an insurance company that verifies the existence of an insurance policy. It summarizes the key aspects and conditions of the policy, such as the type of coverage, the policy limits, and the effective dates.

Businesses and organizations often require COIs when they contract with other businesses or organizations. This ensures that the contracting parties are protected in the event of a loss.

Workplace Safety and Insurance Board or WSIB

The Workplace Safety and Insurance Board (WSIB) is a government agency in Ontario that provides workers’ compensation benefits to employees who are injured or become ill due to their work. The WSIB also provides health and safety information to employers and workers. Note that WSIB covers workers’ compensation, not liability. WSIB premiums are based on payroll.

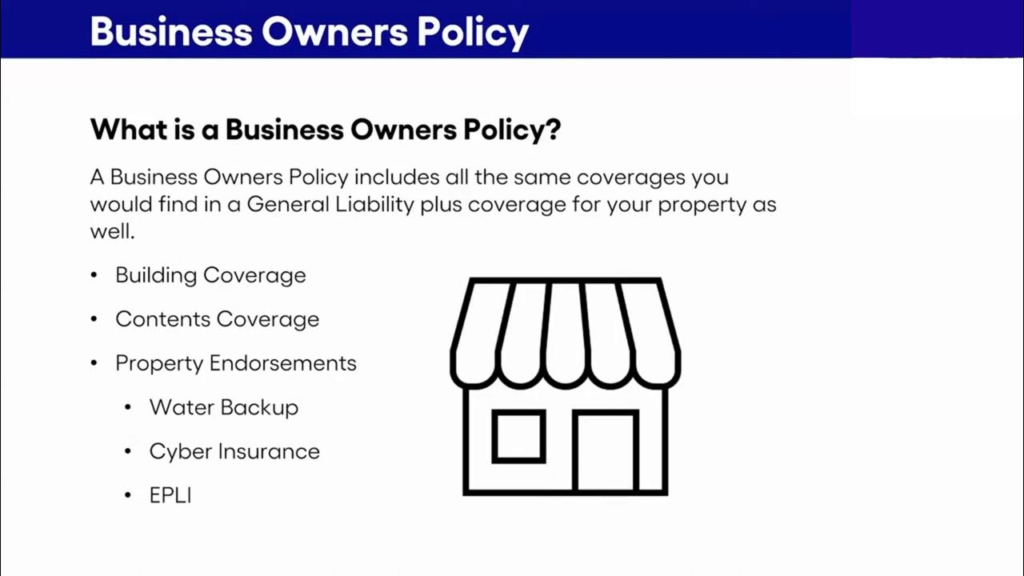

Business Owners Policy (or BOP)

BOPs are typically sold by insurance companies as a package policy, meaning they cover multiple types of risk in a single policy. This can save businesses money on their insurance premiums, as they do not need to purchase separate policies for each type of risk.

Have a complete (detailed) inventory at all times.

If your equipment is damaged or stolen, having a detailed inventory will help your insurance company assess the value of your loss and reimburse you accordingly. Additionally, it can assist you in identifying gaps in your coverage and accounting for depreciation. Be sure to include each piece of equipment’s make, model, and serial number to make the claims process more manageable.

Insurance agent vs. an Insurance broker

An insurance agent and an insurance broker are both professionals who can help you find and purchase insurance. However, there are some key differences between the two.

An insurance agent works for an insurance company. They sell the company’s products and services to potential customers. Agents typically deeply understand the company’s products and services and can help you find the right coverage for your needs.

On the other hand, an insurance broker does not work for any particular insurance company. They are independent contractors who represent a variety of insurance companies. Brokers have access to a broader range of products and services than agents, and they can help you find the best coverage for your needs from multiple companies.

Essential Facts to Know Before Purchasing Any Insurance:

- Only full-time employees are covered by your landscaping insurance policy up to its specified limit. It’s recommended you only hire part-time subcontractors who have insurance.

- Commercial auto insurance will not cover the theft of tools or equipment from that personal vehicle. Personal vehicles used for work are not covered for theft or fire during commercial use.

- If you operate your landscaping business from home and store equipment in a garage or shed, home insurance will not protect you in the event of theft or loss. You may need commercial property insurance.

- Even if you accidentally damage your client’s property, they may wish to sue you rather than go through their insurance.

- Claims might be subject to depreciation.

- Landscapers need at least commercial general liability insurance before going into business.

- List all the lawn mowing and landscaping services you offer. Insurers typically classify mowing, blowing, weeding, and edging as ‘basic lawn care. So if that’s all your company offers, that’s how you’ll be classified for insurance purposes. But if you also offer services like planting, mulching, irrigation, and trimming trees from ground level, that comes under ‘landscaping’. While snow removal, masonry, excavation and land grading come under ‘landscaping’, insurers rate them separately.

- General Liability Insurance does not cover worker’s compensation insurance/pay.

- Expenses associated with re-doing the project (time, manpower, materials) are typically beyond the scope of your general liability coverage.

- Landscaping insurance cost more than other contractor insurance.

- Injury claims are more common in landscaping contracts than in other businesses.

- You should ensure a “hold harmless” agreement benefits your business.

- You can always file a complaint with the Govt if you have an issue with your insurance provider.

Characteristics/what to look for/how to choose

Prompt claim resolution: This is one of the most important factors to consider when choosing an insurance deal. If you ever have to file a claim, you want to ensure that it will be resolved quickly and fairly.

24/7 claims resolution: This is especially important for contractors who work long hours or may be working on projects requiring them to be on-call. You want to be able to file a claim at any time, day or night, and know that it will be handled promptly.

Flexible payment options are another crucial factor, especially for contractors with fluctuating incomes. You want to pay your premiums in a way that is convenient for you, whether monthly, quarterly, or annually.

Flexibility to add-ons and upgrade/downgrade: This is an excellent feature if your business grows or your needs change over time. You want to add or remove coverage as needed without starting a new policy.

Legal assistance and risk management assistance: This valuable service can help you protect your business from legal liability and manage risks. If you have any questions or concerns, you will have access to experts who can help.

Personalized to your company: This is a great way to ensure you get the coverage you need. Your insurance company will work with you to understand your business and risks, and they will customize a policy that is right for you.

Transparency every step of the way is essential for peace of mind. You want to understand your policy and coverage and know what to expect if you ever have to file a claim.

By considering these factors, you can be sure to find an insurance deal that is right for your business and your needs.

Additional tips

- Get quotes from multiple companies: This will help you to compare coverage and prices.

- Read the fine print: Ensure you understand your policy’s terms before signing it.

- Ask questions: If you have any questions, ask your insurance agent.

- Review your policy regularly: Your needs may change over time, so it is essential to review it regularly to ensure it still meets your needs.

Conclusion

Landscaping insurance is a vital protection for any landscaping business or contractor. It can protect you from various risks. Don’t let your hard work go to waste because of an unfortunate incident. Get insured today and enjoy peace of mind while you grow your landscaping business.